As an employer, navigating health insurance can feel like a maze of rules and must-knows – especially for employer-sponsored plans. When you’re choosing coverage for your team, here are five essentials you can’t afford to miss.

Health Insurance for Business Owners: What Every Employer Should Know

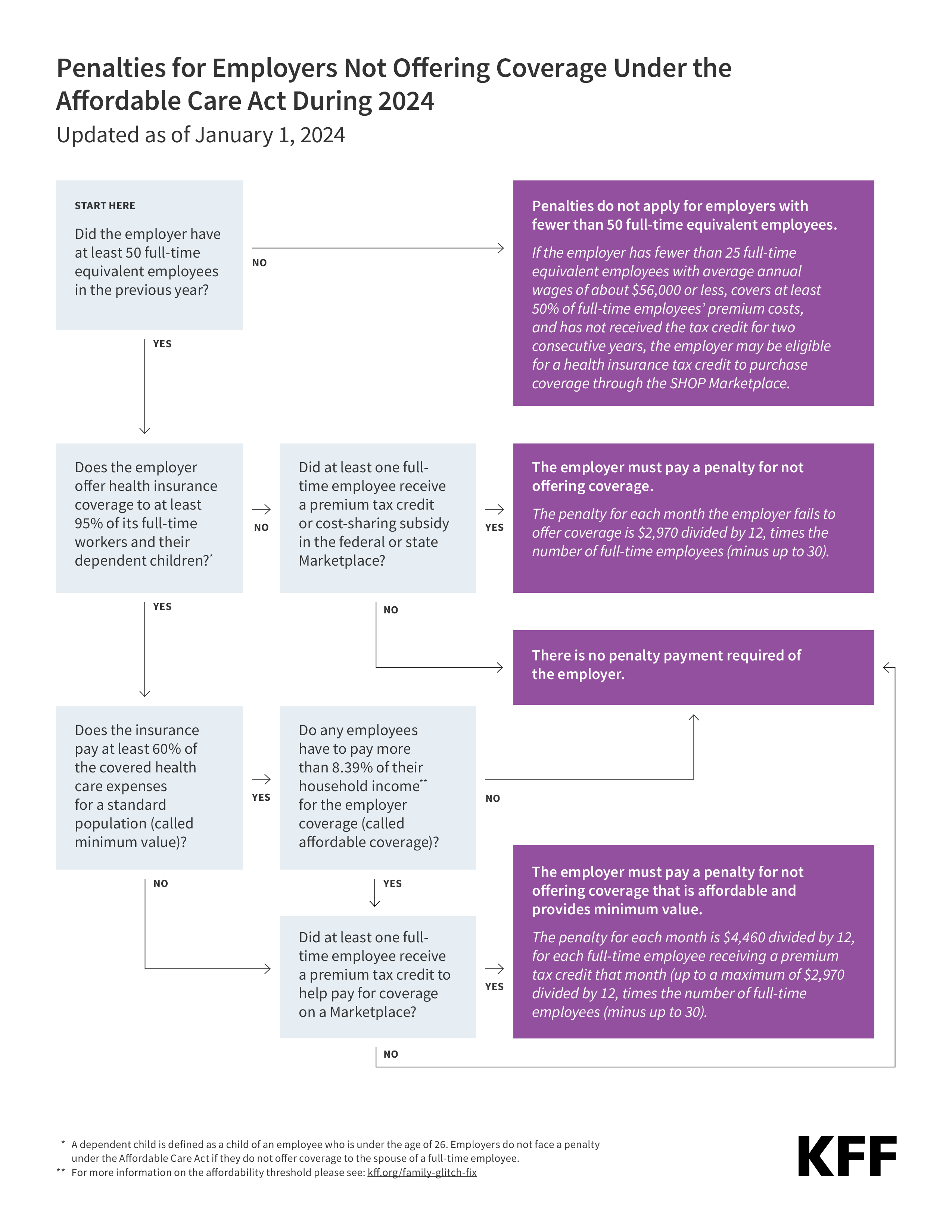

1: The Affordable Care Act Mandates Health Insurance – But Not for Every Employer

Although we don’t yet know how the election will affect Congress’s decision in 2025 regarding a repeal or update of the Affordable Care Act (ACA), it remains in effect for now. The ACA’s Employer Shared Responsibility Provision (ESRP) mandates that businesses with 50 or more full-time or equivalent employees must provide health insurance. This coverage must be “affordable” and offer minimum value to 95% of full-time employees and their dependents, including children through age 25. Businesses not offering qualifying coverage could face penalties, as detailed in the next section.

For smaller employers (with fewer than 50 full-time/full-time equivalent employees), there is no requirement to offer employees health insurance. However, some California employers choose to do so to help employees satisfy the California individual health care mandate. Some smaller employers might also choose to offer health coverage for the reasons mentioned in point 5 below.

2: There Are Penalties for Not Offering Health Insurance to Employees

Applicable Large Employers (ALEs) that do not provide health benefits to their workers may face penalties if coverage is not offered to 95% of eligible full-time employees and dependents, or if it does not meet minimum value and affordability standards.

The “affordability” of coverage is based on the share of premium paid by employees for employee-only coverage in relation to the employee’s household income. In 2024, the guiding percentage was 8.39%; in 2025, it will be 9.02%. For more information, read the “Safe Harbor” overview published by Paylocity, an online HR and payroll firm.

KFF, formerly known as the Kaiser Family Foundation, published an infographic in 2024 that provides a summary of how ACA penalties apply for ALEs and businesses with fewer than 50 full-time equivalent employees.

3: The Tax Benefits of Offering Coverage

Did you know that offering health insurance to your employees can boost your company’s tax savings? If you’re not already providing this benefit, it’s time to consider how deducting coverage costs could work in your favor.

Contributions you make on behalf of your employees for health insurance and other benefits are usually deductible. In most situations, your business can deduct 100% of the premiums paid. Ask your accountant or tax advisor for details.

There’s also a federal Premium Tax Credit that could apply if your business has fewer than 25 full-time equivalent employees and it meets other eligibility guidelines. For details on this program, visit the Internal Revenue Service (IRS) website and read the 2024 updated fact sheet.

If you offer employees a Premium Only Plan (POP), that will reduce your company’s payroll taxes, lower your workers’ compensation premiums, and increase your employees’ take-home pay. When your employees’ share of eligible insurance premiums is paid with pre-tax dollars, they have lower FICA, federal, and state tax deductions on their paychecks. It’s a win-win.

4: Provider Networks Matter: Ensure You and Your Employees Can Access the Facilities You Want and Need

Ask your employee benefits or insurance broker about the health care provider networks linked to each health plan you’re considering. This is crucial if you have ongoing care needs. For instance, if you or an employee has a chronic health condition like heart disease, high blood pressure, or diabetes, maintaining access to your current doctor or specialist may be important. Also, check if the plan covers necessary prescription drugs.

5: Health Insurance Can Help You Attract and Retain Employees – Without a Huge Price Tag

According to numerous surveys, health insurance consistently ranks as one of the most sought-after employee benefits. Employers of all sizes recognize the value of health insurance when it comes to employee recruitment and retention. The Society of Human Resource Management (SHRM) found in 2024 that most employers (97%) offer some kind of health plan to employees. A majority (82%) offer a Preferred Provider Organization (PPO) plan. Sixty-three percent offer high deductible health plans (HDHPs) paired with a Health Savings Account (HSA), health reimbursement arrangement (HRA), or Flexible Spending Account (FSA).

Eighty-eight percent of employees consider health benefits to be “very important” or “extremely important.”

Don’t let health insurance costs hold you back. With CaliforniaChoice, you can give your employees the health coverage they want while keeping your expenses in check.

Through Defined Contribution, you can select a Fixed Percentage or a Fixed Dollar Amount toward the cost of employees’ coverage. If you select a Fixed Percentage, you can choose from 50% to 100% of the cost of a specific health plan or benefit. If you choose a Fixed Dollar Amount, you select what amount you want to contribute to employees’ health insurance premiums each month.

With CaliforniaChoice, employees have the freedom to choose from 100+ options from a variety of premier health plans. If an employee chooses coverage that costs more than you’re contributing, the employee simply pays the difference. Plus, at renewal, you can adjust your contribution amount or continue the same contribution for another 12 months.

Talk With a Broker to Learn More

If you’re unsure about your next step, contact an employee benefits broker. A broker will help you compare options and choose the right health plans that fit your employees’ needs and your company’s budget.